During Q3’2018, the real estate sector recorded an array of activities across all themes supported by (i) continued demand for investment property from multinational individuals and the growing middle class, (ii) Kenyan Government efforts towards enabling the environment for developers through key statutory reforms such as National Land Use Policy, and initiatives such as the National Housing Development Fund set to fund public-private partnerships in delivery of affordable homes, and for end users such as the proposed stamp duty exemption for first time home buyers, (iii) the expanding middle class, and (iv) continued infrastructural improvements.

The key challenges that continue to face developers and end users include: (i) Access to financing with private sector credit growth coming in at 4.3% as at June 2018 compared to a five-year average of 14.0% for the period 2013 to 2018, (ii) high land and construction costs, especially in Nairobi and its metropolis, and (iii) oversupply in selected sectors such as office and retail space with an oversupply of 5.7mn SQFT and 2.0mnSQFT, respectively.

- Industry Reports:

The Kenya National Bureau of Statistics (KNBS) released their Gross Domestic Report Q2’2018, where the key take-outs for the real estate sector were:

- The construction sector recorded slower performance growing by 6.1% in Q2’2018, 1.1% points lower than 7.2% in Q1’2018, and 3.4% points lower than 9.5% growth recorded in Q2’2017 while the consumption of cement dropped by 6.8% in Q2’2018. We attribute the decline to the reduction in development activity particularly in the commercial sector as developers await the absorption of the existing surplus stock of office and retail space with an oversupply of 4.7mn SQFT and 2.0mnSQFT, respectively according to Cytonn Research. Despite the slowed activities, the sector’s growth was supported by the ongoing construction of the second phase of the Standard Gauge Railway (SGR). The KNBS report highlighted a 12.4% increase in credit to the construction industry, a reflection that the sector remained vibrant during the quarter despite being 3.4% points slower than Q2’2017, and,

- The real estate sector grew by 6.6% in Q2’2018, 0.2% points lower than 6.8% in Q1’2018, and 0.6% points higher than the 6.0% growth recorded in Q2’2017, and we attribute the growth to renewed investor confidence, and thus investments in real estate following the improved macro-economic environment.

Source: KNBS

According to KNBS, the real estate and construction sectors contribution to GDP declined to 12.7% in Q2’2018 compared to 14.0% during Q1’2018. We attribute the decline mainly to the 3.4% points decline in activities in construction sector. We however expect the trend to reverse driven by; (i) economic recovery with the GDP growing at 6.3% in Q2’2018, higher than the 4.7% recorded in Q2’2017, and (ii) increased focus on affordable housing as part of the Big 4 Agenda with several projects set to be launched in various parts of the country in the coming months.

- Residential Sector:

The residential sector continued to record activity during Q3’2018, as we witnessed new developments especially in regard to the affordable housing initiative as part of the Kenya Government’s Big 4 Agenda. To this end, the key highlights included:

- The National Government invited bids from both international and local developers to build 1,500 affordable residential units at Nairobi’s Park Road estate situated in Ngara for low–income earners, expected to be delivered within 36-months. The government plans to achieve this through Public-Private Partnerships (PPP’s) where the government’s role is to provide the land while the developer is tasked with the role of designing, funding and constructing the units. For more information, please see Cytonn Weekly #34/2018,

- Nairobi Lands, Urban Renewal and Housing County Executive, Mr. Charles Kerich, announced that the implementation of the Nairobi Urban Regeneration Plan would start in September 2018 in Pangani Estate, where a developer known as Technofin was expected to break ground. However, of key to note is that this is yet to be actualized due to unclear and unsatisfactory methods of resettling the residents of Pangani. For more information, please see Cytonn Weekly #31/2018, and

- Co-operative Bank announced that it will invest Kshs 200.0 mn worth of share capital in the Kenya Mortgage Refinancing Company (KMRC), in support of the facility, which is aimed at boosting mortgage financing in Kenya by increasing liquidity for primary lenders. The facility is also expected to receive Kshs 15.1 bn seed funding from the World Bank, and Kshs 1.5 bn from the National Treasury. For more information, please see Cytonn Weekly #31/2018.

To support the affordable housing initiative, H.E. President Uhuru Kenyatta signed into law various bills with an aim of supplementing the budgetary needs of the affordable housing initiative and also boosting offtake for first-time home buyers and thus, increasing the rate of home ownership in Kenya (currently home ownership rate is 26.4% in urban areas and 89.5% in the rural areas, Kenya National Bureau of Standards). These include;

- The Financial Bill 2018, which includes a clause on employees’ contribution to the National Housing Development Fund, as proposed in the National Budget reading for 2018/2019. As per the clause, employees shall be contributing 1.5% of their gross salary to the fund, while employers top this up with a similar amount,

- The amendment of the Income Tax Act that will allow buyers get a 15.0% tax relief up to a maximum of Kshs 108,000 p.a., or Kshs 9,000 p.m., under the newly introduced Affordable Housing Relief section, and,

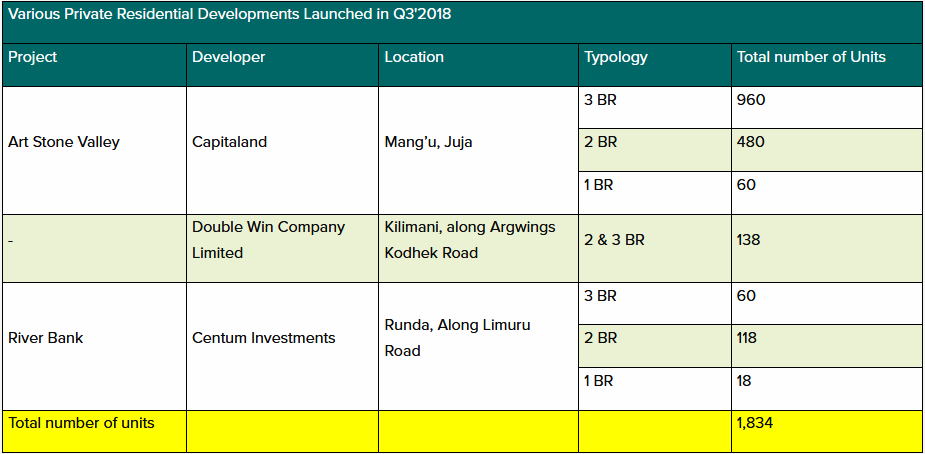

- The amendment of the Stamp Duty Act, which will now exempt first time home-buyers under the affordable housing scheme from paying the Stamp Duty Tax, normally set at 2.0% – 4.0% of the property value. For more information, please see CytonnWeekly#28/2018.These advancements are commendable and in our view are a testament to the Kenyan Government’s commitment to delivering the promise of affordable homes to Kenyans, and we anticipate the launch of various projects especially in the Nairobi, Kiambu, Mombasa and Kisumu Counties in the coming months. However, we expect the lack of an attractive public-private partnership (PPP) package for private developers to remain as the biggest impediment to the delivery of the projects. This is due to the persistent challenges that hinder the success of PPPs in Kenya such as (i) persistent red tape during government approval processes, (ii) equivocal profit-sharing strategies for the private partners, and (iii) long and extended time-frames that tend to characterize PPP projects, thus making them unattractive to private developers.In the mid and high-end market segment, investor appetite remains strong as we have continued to see more private developers coming into the market, such as (i) the recently launched Art Stone Valley project by Kenya-based firm, Capitaland, in partnership with Dubai-based investment firms, that is, Abu Dhabi Investments, Emirate Homes Group, Royal Investments Group; (ii) Double Win Company Limited, a real estate firm, which announced plans to put up a residential complex along Argwings Kodhek Road in Kilimani; while, (iii) Centum, an investment firm in Kenya, announced plans to break ground on Riverbank Apartments within their Two Rivers Mixed Use Development based in Runda. The summary of these projects is as below:

Read More on Cytonn Real Estate Report